Tushit Pandey

Tushit Pandey

Subscribe to stay ahead with expert insights on ESOPs, smart ownership strategies, and more!

Editor’s Note:- The use of ESOPs as a tool for attaining Minimum Public Shareholding in listed companies is made simpler in this article. Every organization has a different set of circumstances, particularly when it comes to promoter shareholding, the size of the ESOP pool, and compliance deadlines. When creating MPS strategies, always consult regulatory experts and use this as a guide rather than legal advice.

If you have ever sat in a boardroom where deadlines, equity, and compliance collide, you are aware that Minimum Public Shareholding (MPS) is a pressure point rather than merely a rule. Legal teams start juggling notices, CFOs start losing sleep, and everyone starts asking the same question

"How do we increase public shareholding without rattling the market?" - when promoter ownership is too high, and deadlines draw near.

Offer for Sale (OFS), Qualified Institutional Placement (QIP), and Institutional Placements are the typical suspects that many listed companies instantly consider. However, one path is frequently disregarded, and paradoxically, it is the one that fortifies the business from the inside out:

When carefully crafted, ESOPs enhance employee ownership, trust, and alignment in addition to helping a business comply with legal requirements. And the magic is there.

All publicly traded companies must maintain a minimum of 25% public shareholding, according to SEBI. This figure is not arbitrary; rather, it serves to maintain a healthy level of liquidity and prevent promoters from exerting undue control.

This implies that a compliance timer is running if promoters collectively hold more than 75%.

Even though it seems straightforward, a lot of businesses fall short of MPS due to

However, how businesses handle it is more important than the rule itself.

Here’s the part most companies miss

ESOP-allotted shares given to non-promoter employees are counted as public shareholding.

This is clearly stated under SEBI’s Share-Based Employee Benefits (SBEB) Regulations.

Therefore, every share that employees exercise in their ESOPs

All without saturating the market with shares all at once.

Something changes culturally when workers perceive that the company wants them to own a genuine portion of the company rather than merely follow a rule. Workers start acting more like builders than spectators. Additionally, the business acquires a base of genuinely concerned internal shareholders.

To bring this down to earth, let’s look at real numbers that affect actual companies

Startup and tech‑company practice guides commonly describe employee option pools in the range of about 10–20% of total company equity, especially in earlier‑stage firms.

This may sound small, but in companies with a tight MPS gap, say 2–3%, ESOPs can close it entirely.

A widely used benchmark in practice is that many high‑growth listed companies and late‑stage startups reserve a high‑single‑digit to low‑teens percentage of their share capital for employee equity plans, with the exact pool size varying by stage and sector rather than being a fixed global statistic.

This is the same pool that can be leveraged to increase public shareholding through exercises.

Publicly available startup and compensation guides show that equity is widely used as a retention and attraction tool, especially in tech and other high‑skill sectors. Still, they focus on pool sizes and grant levels. For example, 10–20% employee pools and 0.25–3% for early hires.

This means ESOPs don’t just help compliantly shift ownership; they actively keep critical teams stable during compliance pressure.

Everyone wins without panic-selling or overnight actions.

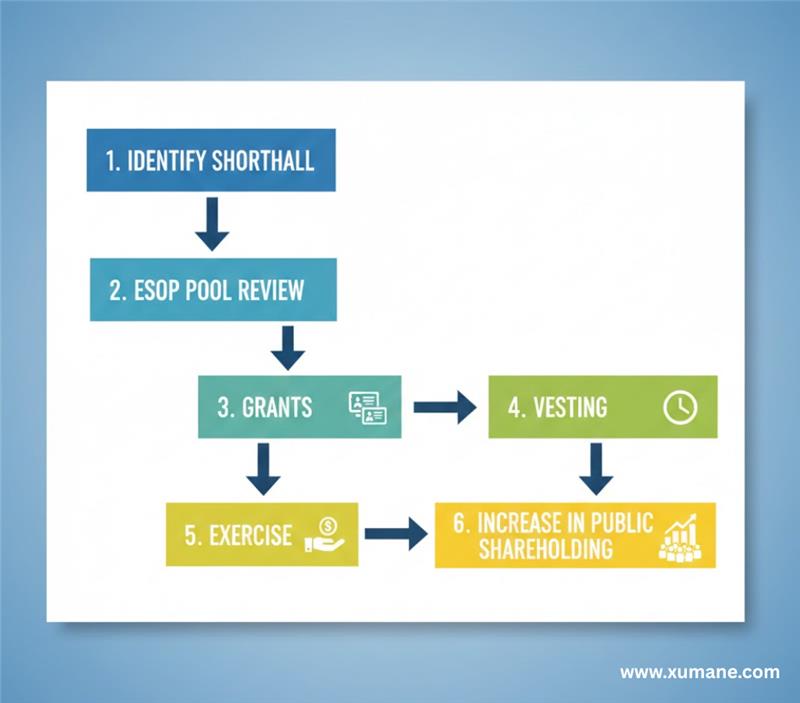

A listed company may take the following action if it notices that its share price is falling below 25%:

To find the shortfall, start with an exercise. Next, examine the current ESOP pool. Refresh or expand it with shareholder approval if necessary. Next, allocate ESOP grants to qualified non-promoter staff members. New shares are issued and immediately added to the public shareholding when employees eventually exercise these vested options. This gradual change minimizes market disruption while assisting in the restoration of MPS.

Also, ESOPs cannot be exercised immediately on grant. A minimum of 1 year cliff period is required from the grant date for the first vesting of options to happen.

If the company needs guidance, NSE maintains a compliance resource page .

ESOP-driven MPS correction occurs gradually, in contrast to OFS or public offers. This prevents promoters from abruptly selling a sizable portion of shares, protects the stock price, and compensates employees.

Through ESOPs, workers become stakeholders rather than just wage earners.

When applied to MPS

Every approach to MPS correction has repercussions.

ESOPs are the only strategy that, rather than merely resolving a regulatory issue, strengthens the organization internally.

Because of this, more publicly traded companies are using ESOP allotments as a strategic, cultural advantage rather than just a solution.

There is no bureaucratic barrier to minimum public shareholding. It protects liquidity, transparency, and market fairness. ESOP allotments are unique because they address the issue while enhancing the company's long-term goals, even though there are numerous mechanical ways to raise public shareholding.

Businesses gain depth when employees take on the role of shareholders. ESOP Compliance becomes more seamless. Ownership expands. Additionally, businesses that treat their employees as long-term partners rather than as a line item in payroll are rewarded by public markets.

ESOPs assist businesses in fulfilling SEBI's requirements, but more significantly, they give employees a sense of ownership.

That kind of obedience fosters loyalty rather than fear.

Yes, as long as the employee is not part of the promoter group.

It can be slower than OFS, but it avoids market shocks and boosts employee morale.

Yes, any ESOP pool expansion requires a special resolution.

For small-to-moderate gaps (1 to 5%), yes. For larger gaps, ESOPs often complement other methods.

Generally, yes, investors prefer structured, predictable dilution over sudden block sales.

Related Content